ESG, ESRS and CSRD are in the spotlight in this article. Much is being written about them. And yet we still receive many questions from concerned customers. Do we need ESG reporting? When do we need it? Can we do this with Power BI? We shed some light on the subject and explain what you need to know as an SME manager: What does ESG, ESRS and CSRD mean? Who needs it and why?

What is ESG?

ESG stands for Environment, Social and Governance. ESG is not a regulation. ESG is a topic, or an umbrella term, that generally stands for sustainable management.

The abbreviation ESG has been used in asset management for a number of years. Some financial products try to differentiate themselves from the competition by using the abbreviation ESG: they only invest in companies that are sustainable and socially responsible.

But how do you define sustainability and social corporate governance? This is where ESRS comes into play.

What is ESRS?

ESRS stands for European Sustainability Reporting Standard. It is a standard that defines exactly how to calculate the sustainability of a company. The ESRS standards are defined by EFRAG (an EU-affiliated institution) and are still being further developed. The EU has approved the ESRS standards as part of the CSRD (see below) as of June 2023.

However, only the ESRS standards for large companies have been adopted so far. Simplified ESG reporting will be sufficient for SMEs and foreign companies. However, as of 2023, this has not yet been precisely defined.

CSRD please what?

CSRD stands for Corporate Sustainability Reporting Directive. This is the EU directive that prescribes how companies must report aspects of sustainability.

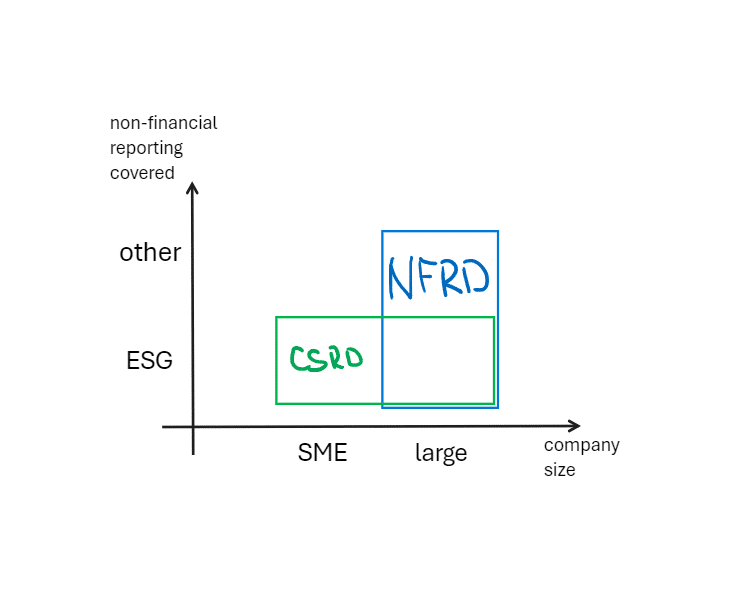

NFRD vs CSRD

NFRD stands for Non-Financial Reporting Directive. It is an EU directive that existed before the CSRD. It stipulates how a company must report non-financial aspects for large companies. Sustainability is a part of these non-financial aspects, but only a part. NFRD is therefore more comprehensive than CSRD, but only applies to large companies.

CSRD, on the other hand, does not only apply to large companies, as we will see later. But the scope of the CSRD is smaller, as it only concerns the sustainability of a company.

ISSB, GRI

In addition to ESRS, there are other ESG standards. The most important ones are ISSB and GRI. Both are international standards that go beyond the EU. The EU is endeavoring to merge the standards so that international companies can report in a consistent and consolidated manner. For the purposes of this article, however, we will immediately forget about the ISSB and GRI. After all, we have enough abbreviations as it is.

Overview

So, to summarise:

- ESG is the topic

- ESRS are the reporting standards that the

- EFRAG - an EU institution - has developed

- CSRD is the law that prescribes which companies must report in accordance with ESRS

Or even simpler: The CSRD stipulates that EU companies must carry out their ESG reporting in accordance with the ESRS standard.

Which companies must prepare sustainability reports in accordance with the CSRD?

The CSRD stipulates that the following companies must prepare an ESG report in accordance with ESRS

- from 2024:

- listed companies with more than 500 employees

- Banks and insurance companies with more than 500 employees

- from 2026: SMEs that are active on the capital market and fulfil at least two of the following criteria:

- Balance sheet value of more than EUR 20 million

- Turnover of more than EUR 40 million

- More than 250 employees

- from 2028: listed companies that are not headquartered in the EU and fulfil at least two of the following criteria

- Turnover over EUR 150 million

- a subsidiary in the EU that generates at least EUR 40 million in turnover

What applies to SMEs?

As the managing director of an SME, you are probably wondering: Am I affected by the ESRS? And if so, from when?

Here is the summarised answer:

- SMEs are only affected if they are listed on a stock exchange or if they are otherwise active on the capital market, e.g. if they issue traded bonds (debentures).

- SMEs have a two-year opt-out period. If they make use of this, they do not have to report in accordance with ESRS until 2028.

- the ESRS standards for SMEs will be less demanding than those for large companies. However, this simplified reporting is not yet precisely defined. It is currently being developed by EFRAG

Voluntary ESRS reporting for SMEs

In addition to the simplified SME standards, EFRAG is working on an even simpler standard for SMEs that are not required to report. This voluntary standard will be easy to fulfil.

But why on earth would I voluntarily go to the effort of voluntarily subjecting myself to regulation?

Well, an ESG report can give your company a label for particularly sustainable business practices. This can be a great advantage.

For example, proven sustainability strengthens your employer branding. Environmentally conscious employees can identify with your company. Your company stands out as sustainable to good candidates.

Your business customers will also thank you. They also have to report on the sustainability of the goods they buy. It is therefore an advantage for your B2B customers to purchase their goods and services from an SME that operates sustainably.

And finally, it is also an advantage for your brand in general: a company that is committed to sustainability is perceived more favourably than a dirt slinger.

ESRS under the magnifying glass

But what does the ESRS standard contain for reports and KPIs?

ESRS defines reports from four groups:

- General

- Environment

- Social (Social)

- Governance

The four groups are divided into a total of 12 areas:

| Group | Area | Topic |

|---|---|---|

| General | 1 | General requirement |

| General requirement | 2 | General reporting requirements |

| Environment | E1 | Climate |

| Environment | E2 | Pollution |

| Environment | E3 | Water |

| Environment | E4 | Biodiversity |

| Environment | E5 | Resource consumption |

| Social | S1 | Own employees |

| Social | S2 | Workers in the value chain |

| Social | S3 | Affected communities |

| Social | S4 | Consumers and consumers |

| Corporate governance | G1 | Corporate governance |

As we can see, the ESRS is not just about CO2 emissions (E1), but about many other topics.

Nevertheless, E1 is the best-known area of ESRS. That's why we want to take a closer look at this best-known of all ESG areas below.

E1 - Climate

Each of the 12 areas in the ESRS is subdivided again. Area E1 (Climate), for example, is subdivided into nine directives (DR) from the categories Strategy and Metrics.

The directives for area E1 are

- Strategic directives

- DR E1-1 Transition plan

- DR E1-2 Strategies

- DR E1-3 Measures

- Metrics

- DR E1-4 Targets related to mitigation

- DR E1-5 Energy consumption and energy mix

- DR E1-6 Greenhouse gas emissions

- DR E1-7: Compensation (certificates)

- DR E1-8: CO2 pricing (carbon pricing)

- DR E1-9 Financial effects

DR E1-6: Greenhouse gases

Let's go even deeper and take a closer look at the directive DR E1-6, greenhouse gases.

So here we are:

ESRS -> Environment -> E1 (Climate) -> E1-6 (Greenhouse gases).

According to ESRS, how do you have to report how much CO2 a company has emitted?

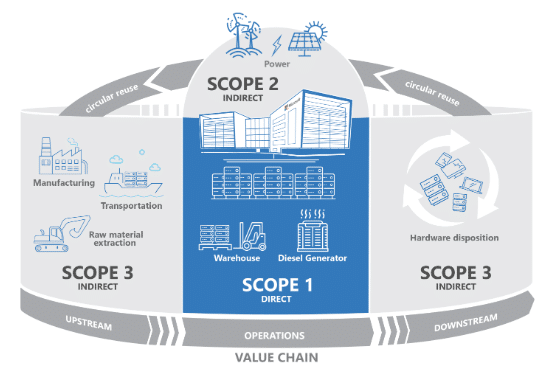

According to DR E1-6, greenhouse gas emissions are divided into three scopes:

- Scope 1: direct production emissions (e.g. diesel generator)

- Scope 2: indirect production emissions through purchased energy sources (e.g. electricity)

- Scope 3: Indirect non-production emissions

- Upstream:

- purchased services and goods

- Employees travelling to work

- Business trips

- Waste

- Downstream:

- Utilisation of the goods sold

- Recycling and disposal of the goods sold

- Distribution

- Upstream:

These scopes do not overlap. For a given company, an issue is either in category 1, 2 or 3.

Scope 1 often flows into consumer goods as "grey energy".

Dashboard

And here it is, our "Dashboard of the Month": Microsoft has a free dashboard available for Power BI that calculates the emissions generated by your company's use of M365.

The following dashboard with sample data explains the report and the underlying calculation:

As a reminder, we are now in a tiny corner of your company's ESRS reporting. Specifically:

ESRS -> Environment -> E1 (Climate) -> E1-6 (Greenhouse gases) -> Emissions from M365

This is therefore not a complete ESRS report. It is only the emissions caused by your company's use of the cloud.

If you have access to Power BI, you can install the Power BI template free of charge and display your own company's data.

To do this, proceed as follows:

- go to https://app.powerbi.com

- log in

- click on Apps

- Search for "Emissions Impact Dashboard for Microsoft 365"

- "Get It Now"

After a few hours, you will see the emissions data that your company generates with Microsoft 365.

How complex is the implementation of ESRS?

It is not time-consuming to calculate CO2 emissions for individual areas. Implementing the entire ESRS standard, on the other hand, is a different matter. Imagine you have to collate the data from the dashboard above from a large number of business units and activities. That's a lot of work!

ESRS is a big standard. Both the procurement of data, the calculation of metrics and the creation of reports are time-consuming. It remains to be seen how high the requirements for SMEs will be.

ESG software

Due to the complexity of ESRS, it currently makes no sense to set up ESG reporting from scratch in Excel.

On the other hand, there are a large number of specialised tools. These automatically request the necessary data from the user and guide employees step by step to the required reports.

BARC, a German analyst firm for business software focussing on the areas of data and business intelligence (BI), has compiled a free overview: https://barc.de/research/esg-reporting-tools (registration required).

ESG reporting in Power BI

Microsoft offers several ESG solutions for companies:

- Microsoft Cloud for Sustainability: https://www.microsoft.com/de-de/sustainability/cloud. This is a portal that lists access to various ESG solutions from Microsoft.

- CSRD template in Purview: Purview is Microsoft's data governance solution. The CSRD template is not ESRS reporting, but allows CSRD-compliant provision, tracking and publication of data.

- Project ESG Lake (Preview): This is a solution that focusses on data provision. It is currently in a closed preview.

The collection looks somewhat handmade.

Setting up complete ESRS reporting in Power BI also seems very complex to us.

Tip: What should I do?

Here are our tips:

- If you have to do ESRS reporting in accordance with the CSRD, then you should seek advice from a specialist.

- If you are an SME and do not have to report (for the time being), then it is best to keep up to date. If a voluntary reporting obligation is decided, you will have enough time to implement the requirements.

- If you would like to measure the sustainability of your company before then, please get in touch with us. We may have an idea of how we can estimate greenhouse gas emissions, for example, without having to collect a lot of data.

{kind=link}

{kind=link}

{kind=link}